An event provides additional information about conditions in existence as of the balance sheet date, including estimates used to prepare the financial statements for that period. Events that affect the realization of receivables due to conditions that existed at the balance sheet date. This may occur when trade accounts receivable becomes uncollectible due to a customer filing for bankruptcy after the balance sheet date but before the financial statements are issued. Even though the filing for bankruptcy occurred after the balance sheet date, the customer’s deteriorating financial condition at the time of the balance sheet date is indicative of conditions existing at the balance sheet date. Subsequent events may not be reflected on a company’s balance sheet or income statement.

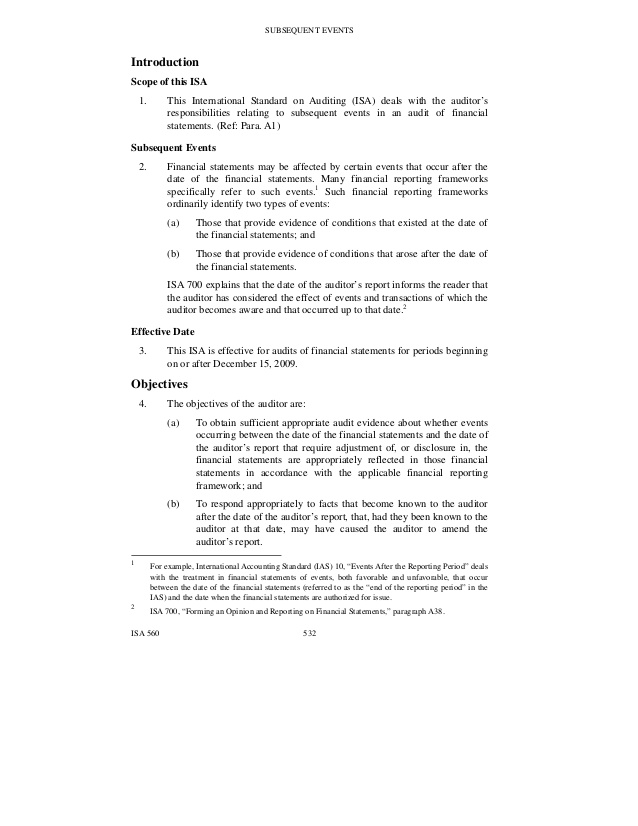

What are the two types of subsequent events?

Subsequent event is the accounting term for a financial transaction that occurs after completion of the balance sheet for a specified period but before the company’s full set of financial statements is prepared.

Answer C. To reissue the 20X1 auditor’s report on financial statements that have been neither restated nor revised, the auditor should use the original report date on the reissued report. Dual dating is used when a subsequent event occurs after the date of the report, but the report has not been issued. The subsequent event is disclosed in the financial statements, and the auditor’s report also includes the date of the subsequent event.

Under these circumstances, the company discloses the contingent liability in the footnotes of the financial statements. If the firm determines that the likelihood of the liability occurring is remote, the company does not need to disclose the potential liability. A contingent liability is a liability that may occur depending on the outcome of an uncertain future event. A contingent liability is recorded if the contingency is likely and the amount of the liability can be reasonably estimated. The liability may be disclosed in a footnote on the financial statements unless both conditions are not met.

Subsequent Events: When Do I Record and When Do I Disclose?

In order to answer this question, it is important to first define what is a subsequent event? A company should disclose the date through which there has been an evaluation of subsequent events, as well as either the date when the financial statements were issued or when they were available to be issued. There may be situations where the non-reporting of a subsequent event would result in misleading financial statements. If so, disclose the nature of the event and an estimate of its financial effect. If a business reissues its financial statements, disclose the dates through which it has evaluated subsequent events, both for the previously issued and revised financial statements.

Subsequent Events Definition

The Financial Accounting Standards Board, the authority entrusted with establishing generally accepted accounting principles, publishes detailed requirements for defining and recording subsequent events in financial records. IAS 10 Events After The Reporting Period contains requirements for when events after the end of the reporting period should be adjusted in the financial statements. The balance sheet, usually prepared monthly, provides a summary of a company’s assets, liabilities and equity. By dating and issuing a balance sheet a company represents that the summary includes all transactions and events recorded through the balance sheet date.

Accountants evaluate financial transactions or events that occur after the balance sheet has been prepared to determine if the events affect the picture reflected in the company’s financial statements. In 2009, the Financial Accounting Standards Board changed elements of its official subsequent event guidance. When should subsequent events, that occur after the balance sheet date but before the financial statements are issued, be recognized in the financial statements or, rather, merely be disclosed in the notes to the financial statements?

The definition of a subsequent events are generally defined as events that occurs after the year end period but before the financial statements have been issued. A subsequent event falls underneath the disclosure principle and can be confusing to many accountants that encounter them. This allows accountants to distinguish separate events and how to write subsequent events disclosure. Certain red flags may appear on financial statements of publicly traded companies that may indicate a business will not be a going concern in the future. Listing of long-term assets normally does not appear in a company’s quarterly statements or as a line item on balance sheets.

Subsequent events definition

- Recognized subsequent events require adjustments to the financial statements, according to the Federal Accounting Standards Advisory Board.

- An example of a recognized subsequent event is if your company resolves a legal case for an amount that differs from the expected liability recorded before the balance sheet date.

Recognized subsequent events require adjustments to the financial statements, according to the Federal Accounting Standards Advisory Board. Recognized events, such as changes to assets or liabilities, add evidence about the financial picture reflected on the balance sheet date and alter the estimates or summarization of the financial information included in the report. An example of a recognized subsequent event is if your company resolves a legal case for an amount that differs from the expected liability recorded before the balance sheet date. A recognized subsequent event that adds information about an existing condition is the write-off of a long-standing overdue account when the customer closes his business or files bankruptcy.

Subsequent Events

Using the reissued report release date, or the current-period auditor’s report date, would extend the auditor’s responsibility for subsequent events to that date. There is a danger in inconsistently applying the subsequent event rules, so that similar events do not always result in the same treatment of the financial statements. These events provide further evidence of conditions that existed on the financial statement date. There was probably evidence of the customer’s financial distress in the prior period, such as a decrease in revenue or a buildup of receivables. The customer’s bankruptcy filing may trigger a write-off for bad debts to be recorded on the balance sheet in the prior period.

Subsequent Events Meaning

The Federal Accounting Standards Advisory Board recommends evaluating financial conditions affected by subsequent events if the information is known prior to issuing the balance sheet or the financial statements. Non-recognized subsequent events do not require adjustments to the financial statements. Such events are those that relate to financial conditions that did not exist on the balance sheet date but arose after the date.

The adjustment of records for subsequent events can improve a company’s financial picture, an important consideration for a business that hopes to attract lenders or investors. The balance sheet is used by the company, investors and others who make decisions based on the company’s financial health. Financial statements, the full set of which is usually released at the end of the company’s fiscal year, include the balance, sheet, income statement, statement of cash flows and, if necessary, supplementary notes.

Companies that are a going concern may defer reporting long-term assets at current value or liquidating value, but rather at cost. A company remains a going concern when the sale of assets does not impair its ability to continue operation, such as the closure of a small branch office that reassigns the employees to other departments within the company. Now assume that a lawsuit liability is possible but not probable and the dollar amount is estimated to be $2 million.

But, when in doubt, companies typically disclose subsequent events to promote transparency in financial reporting. Contact us for more information about reporting and disclosing subsequent events.

Accounting standards try to determine what a company should disclose on its financial statements if there are doubts about its ability to continue as a going concern. In May 2014, the Financial Accounting Standards Boarddetermined financial statements should reveal the conditions that support an entity’s substantial doubt that it can continue as a going concern.

A fire in your company plant that destroys inventory and other assets is a non-recognized subsequent event because conditions did not exist prior to the balance sheet date. Another example is the loss of expected income due to conditions suffered by a client. The Federal Accounting Standards Advisory Board cautions that while adjustments are not required, disclosure of certain non-recognized events might be necessary to avoid issuing misleading financial information. Subsequent event is the accounting term for a financial transaction that occurs after completion of the balance sheet for a specified period but before the company’s full set of financial statements is prepared. Subsequent events clarify information about a business’ financial picture as reflected by the balance sheet, a financial report that includes all transactions through the report date.

Listing the value of long-term assets may indicate a company plans to sell these assets. Accountants use going concern principles to decide what types of reporting should appear on financial statements.