Many accounting terms can get mixed up and blurred together when we try to wrap our heads around the accounting process. So, what are accounting journals?

Accounting journals definition

An accounting journal is defined as a record in which any financial transactions of a company that occurs are entered before they are posted to ledger accounts, also called the book of original entry. Why is it important to record transactions? There are at least several reasons:

- Financial reports measure the performance of your business;

- Manage your cash flow;

- Keep things organized;

- Useful at tax time;

- In case your business gets audited.

Accounting journals are a more efficient way to record transactions compared to the T accounts. They are used for reconciling and transfer to other official accounting records, special accounting journals such as accounting General Ledger. Let’s take a look at accounting journal templates.

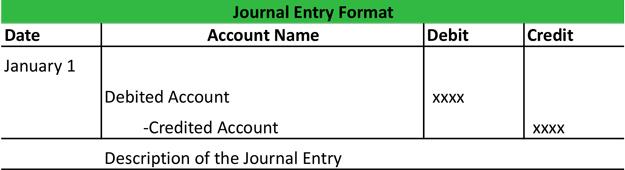

Template 1:

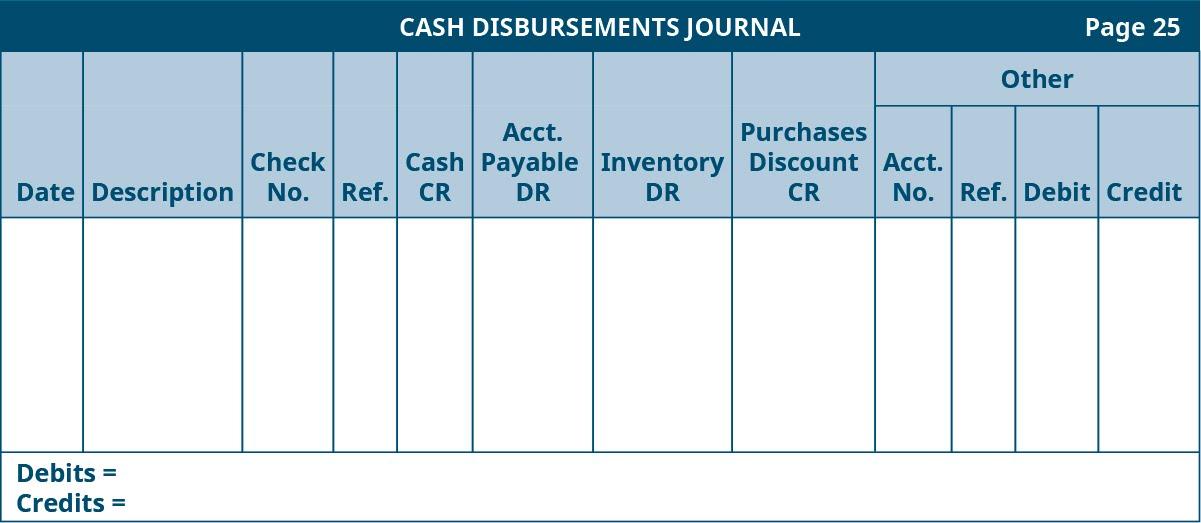

Template 2:

As you can see from the accounting journal examples above, we always record debits first and credits next. It will also have a date and a short description.

There are several types of accounting journals you can come across top accounting journals such as a Sales Journal, Sales Return Journal, Purchases Journal, Cash Receipts Journal, and many others depending on the type of business, etc. Since accounting nowadays is done using computer software, these accounting journals are usually limited to the accounting General Journal.

How to Do Accounting Journal Entries?

Making a journal entry is the first step in the accounting system. The journal entry is a record of financial transactions. So, let’s see how you would make the journal entry using an example.

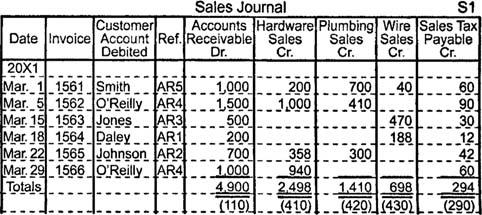

At the top right corner, you can see a journal number that is a unique reference number used to identify the journal. Then, there is the journal entry date. This is the date that the entry is posted. It is important because it affects the accounting period that the transaction is going to show up in.

Next, we might have optional columns, such as invoice number, description, and customer name. It is recommended to include such columns to be able to remember the transaction details. The accounts that are impacted by the journal entry are the required part of each journal. You will see two or more accounts listed here.

IT is important to ensure that the totals of debits and credits for each entry and for the entire period are equal. As you can in in this example, the totals of debit and credit columns match exactly (DR 4,900 = CR 2,498 + 1,410 + 698 + 294).

To identify the debit and credit side in the accounting journal, you should remember that the debit column is always on the left of the accounting entry, and the credit column is on the right. To know whether you need to debit or credit the account recall that debits increase an asset or expense accounts and decrease liability and equity accounts.

Should Journal Entries be Balanced?

If the company is adhering to the double-entry accounting method, then the journal entries would balance. As you have seen from the examples above, this is done with the help of the debit and the credit sides of each journal entry.

This means that every journal entry has to involve at least two accounts. Depending on the type of account affected, you will need to use either a credit or debit entry to increase it and vice versa. The total of debits will always equal the total of credits in each journal entry.

Thus, just as you would have to keep a balance in the accounting equation, you must keep your debits and credits in the accounting journals in balance. If you are using accounting software, there is usually an automatic control that will not allow posting an entry if the debits and credits do not match each other exactly.