Performing a vertical analysis of a company’s cash flow statement represents every cash outflow or inflow relative to its total cash inflows. Vertical Analysis is a form of financial analysis where the line items on a company’s income statement or balance sheet is expressed as a percentage of a base figure. A vertical analysis is also the most effective way to compare a company’s financial statement to industry averages. Using actual dollar amounts would be ineffective when analyzing an entire industry, but the common-sized percentages of the vertical analysis solve that problem and make industry comparison possible. To do that, we’ll create a “common size income statement” and perform a vertical analysis.

- The process is virtually identical to our common size income statement, however, the base figure is “Total Assets” as opposed to “Revenue”.

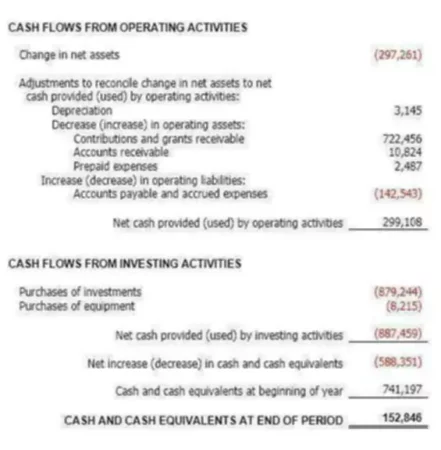

- What we don’t know, and what we can’t know from the vertical analysis, is why that is happening.

- For example, on an income statement, every line item is stated in terms of the percentage of gross sales.

- The information provided by this income statement format is useful not only for spotting spikes in expenses, but also for determining which expenses are so small that they may not be worthy of much management attention.

But we’ll utilize the latter here, as that tends to be the more prevalent approach taken. Upgrading to a paid membership gives you access to our extensive collection of plug-and-play Templates designed to power your performance—as well as CFI’s full course catalog and accredited Certification Programs.

Vertical Analysis of the Income Statement

Salaries and marketing expenses have risen, which is logical, given the increased sales. However, these expenses don’t, at first glance, appear large enough to account for the decline in net income. Investors can use horizontal analysis to determine the trends in a company’s financial position and performance over time to determine whether they want to invest in that company. However, investors should combine horizontal analysis with vertical analysis and other techniques to get a true picture of a company’s financial health and trajectory. On the other hand, horizontal analysis looks at amounts from the financial statements over a horizon of many years. Coverage ratios, like the cash flow-to-debt ratio and the interest coverage ratio, can reveal how well a company can service its debt through sufficient liquidity and whether that ability is increasing or decreasing.

This implies that the new money invested in marketing was not as effective in driving sales growth as in prior years. All of the amounts on the balance sheets and the income statements for analysis will be expressed as a percentage of the base year amounts. For example, the vertical analysis of an income statement results in every income statement amount being restated as a percent of net sales. If a company’s net sales were $2 million, they will be presented as 100% ($2 million divided by $2 million).

For example, if the cost of goods sold has a history of being 40% of sales in each of the past four years, then a new percentage of 48% would be a cause for alarm. The primary difference between vertical analysis and horizontal analysis is that vertical analysis is focused on the relationships between the numbers in a single reporting period, or one moment in time. Horizontal analysis allows investors and analysts to see what has been driving a company’s financial performance over several years and to spot trends and growth patterns. This type of analysis enables analysts to assess relative changes in different line items over time and project them into the future.

Over 1.8 million professionals use CFI to learn accounting, financial analysis, modeling and more. Start with a free account to explore 20+ always-free courses and hundreds of finance templates and cheat sheets. For example, the amount of cash reported on the balance sheet on Dec. 31 of 2018, 2017, 2016, 2015, and 2014 will be expressed as a percentage of the Dec. 31, 2014, amount. The following example shows ABC Company’s income statement over a three-year period. For instance, if a most recent year amount was three times as large as the base year, the most recent year will be presented as 300. Second, a variance analysis determines not only the dollar amount but the direction of change for a given general ledger account.

Horizontal Analysis vs. Vertical Analysis

For example, upper management may ask “how well did each geographical region manage COGS over the past four quarters?”. This type of question guides itself to selecting certain horizontal analysis methods and specific trends or patterns to seek out. Last, a horizontal analysis can encompass calculating percentage changes from one period to the next. As a company grows, it often becomes more difficult to sustain the same rate of growth, even if the company grows in pure dollar size. This percentage method is most useful when identifying changes over a longer period of time where there may be significant deviations from the base period to the current period.

Vertical analysis is used in order to gain a picture of whether performance metrics are improving or deteriorating. Since liabilities and equity represent a company’s funding sources – i.e. how the company obtained the funds to purchase its assets – this part of the analysis can be insightful for understanding where the company’s financing stems from. To reiterate from earlier, dividing by total assets is akin to dividing by the sum of liabilities and equity. Once the historical data from 2021 has been inputted into Excel, we must determine the base figure to use.

Vertical Analysis

If the cost of goods sold amount is $1 million, it will be presented as 50% ($1 million divided by sales of $2 million). On the liabilities and shareholders equity side, we’ve chosen the base figure to be total assets. The standard base figures for the income statement and balance sheet are as follows. This shows that the amount of cash at the end of 2018 is 141% of the amount it was at the end of 2014. By doing the same analysis for each item on the balance sheet and income statement, one can see how each item has changed in relationship to the other items. Depending on which accounting period an analyst starts from and how many accounting periods are chosen, the current period can be made to appear unusually good or bad.

Criticism of Horizontal Analysis

While performing a vertical analysis, every line item on a financial statement is entered as a percentage of another item. For example, on an income statement, every line item is stated in terms of the percentage of gross sales. To perform a horizontal analysis, you must first gather financial information of a single entity across periods of time. Most horizontal analysis entail pulling quarterly or annual financial statements, though specific account balances can be pulled if you’re looking for a specific type of analysis. Horizontal analysis is used in financial statement analysis to compare historical data, such as ratios, or line items, over a number of accounting periods.

Vertical analysis definition

Horizontal analysis is most useful when an entity has been established, has strong record-keeping capabilities, and has traceable bits of historical information that can be dug into for more information as needed. This type of analysis is more specific relevant for analyzing the value we maybe selling or acquiring. With the financial information in hand, it’s time to decide how to analyze the information. You can choose whatever interval (month-over-month, year-over-year, etc.), but each iterative financial statement should be equal distance away regarding when it was issued compared to other bits of financial information. The analysis of critical measures of business performance, such as profit margins, inventory turnover, and return on equity, can detect emerging problems and strengths. For example, earnings per share (EPS) may have been rising because the cost of goods sold (COGS) has been falling or because sales have been growing steadily.

In the current year, company XYZ reported a net income of $20 million and retained earnings of $52 million. Consequently, it has an increase of $10 million in its net income and $2 million in its retained earnings year over year. The assets section is informative with regard to understanding which assets belonging to the company constitute the greatest percentage.

First, a direction comparison simply looks at the results from one period and comparing it to another. For example, the total company-wide revenue last quarter might have been $75 million, while the total company-wide revenue this quarter might be $85 million. This type of comparison is most often used to spot high-level, easily identifiable differences.