Equity accounts may include retained earnings and dividends. Revenue accounts can include interest, sales or rental income.

In the chart of accounts, the Cash account is a current asset account. Office Supplies is an operating expense account, and Accounts Payable is a liability account. Asset accounts, for example, can be divided into cash, supplies, equipment, deferred expenses and more.

However, an intermediate account called Income Summary usually is created. Revenues and expenses are transferred to the Income Summary account, the balance of which clearly shows the firm’s income for the period.

Mary Smith, Capital is an owner equity account with a normal balance of credit. If you credit the account you are increasing its balance. Asset accounts normally have debit balances and are debited to increase their balances. Supplies become expenses once a business uses them. However, there’s another case in which a company can treat supplies as an expense instead of as current assets.

Therefore to increase the account you need to CREDIT it. The second reason is that the normal balance for Mary Smith, Capital is a credit balance and to increase its balance, we need to CREDIT the account. Recall that the owner equity account, Mary Smith, Capital is on the right side or credit side of the accounting equation and therefore its balance is normally a credit balance. The owner’s equity account, Mary Smith, Capital, should be CREDITED.

The cash basis of accounting, or cash receipts and disbursements method, records revenue when cash is received and expenses when they are paid in cash. In contrast, the accrual method records income items when they are earned and records deductions when expenses are incurred, regardless of the flow of cash. Accrual accounts include, among others, accounts payable, accounts receivable, goodwill, deferred tax liability and future interest expense. Debits increase the balance of an expense account, while credits decrease the balance of an asset account.

Asset accounts normally have debit balances and a debit will increase asset balances. You should CREDIT an asset to reduce an asset’s balance.

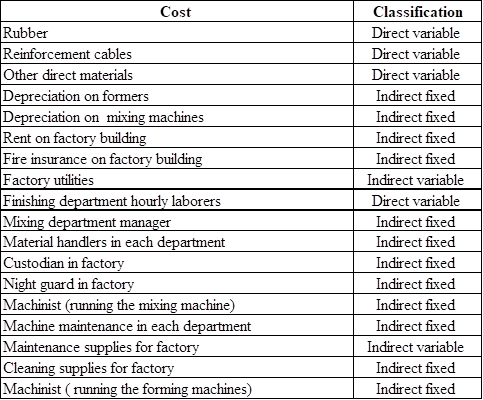

Using depreciation, a business expenses a portion of the asset’s value over each year of its useful life, instead of allocating the entire expense to the year in which the asset is purchased. This means that each year that the equipment or machinery is put to use, the cost associated with using up the asset is recorded. In effect, capital assets lose value as they age. The rate at which a company chooses to depreciate its assets may result in a book value that differs from the current market value of the assets.

It is important for us to consider perspective when attempting to understand the concepts of debits and credits. For example, one credit that confuses most newcomers to accounting is the one that appears on their own bank statement. We know that cash in the bank is an asset, and when we increase an asset we debit its account.

The drawing account normally has a debit balance and should be debited when the owner withdraws assets from the business for personal use. When the owner draws money out of the business, the business will CREDIT Cash. That means the other account involved will have to be debited. Mary Smith, Drawing is a contra owner’s equity account.

Each category can be further broken down into several categories. Revenue is treated like capital, which is an owner’s equity account, and owner’s equity is increasedwith a credit, and has a normal credit balance. The term accrual is also often used as an abbreviation for the terms accrued expense and accrued revenue.

Take Inventory of Supplies

The fundamental accounting equation can actually be expressed in two different ways. A double-entry bookkeeping system involves two different “columns;” debits on the left, credits on the right. Every transaction and all financial reports must have the total debits equal to the total credits.

Are Supplies Credit or Debit?

- The drawing account normally has a debit balance and should be debited when the owner withdraws assets from the business for personal use.

When you credit an account, you enter the amount on the right side of the account. A debit to the drawing account will increase (not decrease) the balance in Mary Smith, Drawing. Hence you debit the account to decrease its balance.

supplies definition

The expense accounts have debit balances so to get rid of their balances we will do the opposite or credit the accounts. Just like in step 1, we will use Income Summary as the offset account but this time we will debit income summary.

By doing so, the supplies are considered an expense immediately from the time of purchase. Companies can do this, even though it goes against accounting standards, because of an accounting principle known as materiality. After closing, the balance of Expenses will be zero and the account will be ready for the expenses of the next accounting period. At this point, the credit column of the Income Summary represents the firm’s revenue, the debit column represents the expenses, and balance represents the firm’s income for the period. After the closing entries have been made, the temporary account balances will be reflected in the Retained Earnings (a capital account).

One reason is that the Cash account was debited (because the company received cash). Therefore, the other part of the transaction needs to be a credit. Closing entries are the journal entries used to transfer the balances of these temporary accounts to permanent accounts. There are five main types of accounts in accounting, namely assets, liabilities, equity, revenue and expenses. Their role is to define how your company’s money is spent or received.

Then how come the credit balance in our bank accounts goes up when we deposit money? The answer is one that is fundamental to the accounting system. Each firm records financial transactions from their own perspective. There are two primary accounting methods – cash basis and accrual basis.

For example, if you pay cash for office supplies and credit the Cash account, the Cash account balance decreases. When using a double-entry accounting system, you must also debit the Office Supplies account, which increases the balance in that account. To debit an account, you make the entry on the left side of the account.

A mark in the credit column will increase a company’s liability, income and capital accounts, but decrease its asset and expense accounts. A mark in the debit column will increase a company’s asset and expense accounts, but decrease its liability, income and capital account.

We need to do the closing entries to make them match and zero out the temporary accounts. Asset accounts normally have debit balances.

In the world of accounting, every business transaction involves at least two accounts. An expense is a cost you incur during the normal operating activities of your business. When you debit office supplies as an expense to an account such as Office Supplies, you would credit a Cash account if you paid for the supplies with cash. But if you use a credit card or receive a billing invoice you have to pay, you record the office expense in the Accounts Payable account.

Then, Income Summary is closed to Retained Earnings. An adjusting entry is a journal entry made at the end of an accounting period that allocates income and expenditure to the appropriate years. Adjusting entries are generally made in relation to prepaid expenses, prepayments, accruals, estimates and inventory. Throughout the year, a business may spend funds or make assumptions that might not be accurate regarding the use of a good or service during the accounting period. Adjusting entries allow the company to go back and adjust those balances to reflect the actual financial activity during the accounting period.

The total debit to income summary should match total expenses from the income statement. On the statement of retained earnings, we reported the ending balance of retained earnings to be $15,190.

We now offer eight Certificates of Achievement for Introductory Accounting and Bookkeeping. The certificates include Debits and Credits, Adjusting Entries, Financial Statements, Balance Sheet, Income Statement, Cash Flow Statement, Working Capital and Liquidity, and Payroll Accounting. It is very unusual that previous expenses already recorded in an expense account will be decreased. However, a CREDIT will reduce the normal debit balances of expenses.

What kind of asset is supplies?

supplies definition. A current asset representing the cost of supplies on hand at a point in time. The account is usually listed on the balance sheet after the Inventory account. A related account is Supplies Expense, which appears on the income statement.

Accounts Receivable is an asset and a CREDIT is needed to decrease its normal debit balance. Mary Smith, Capital is an owner equity account and its normal balance is a credit balance.