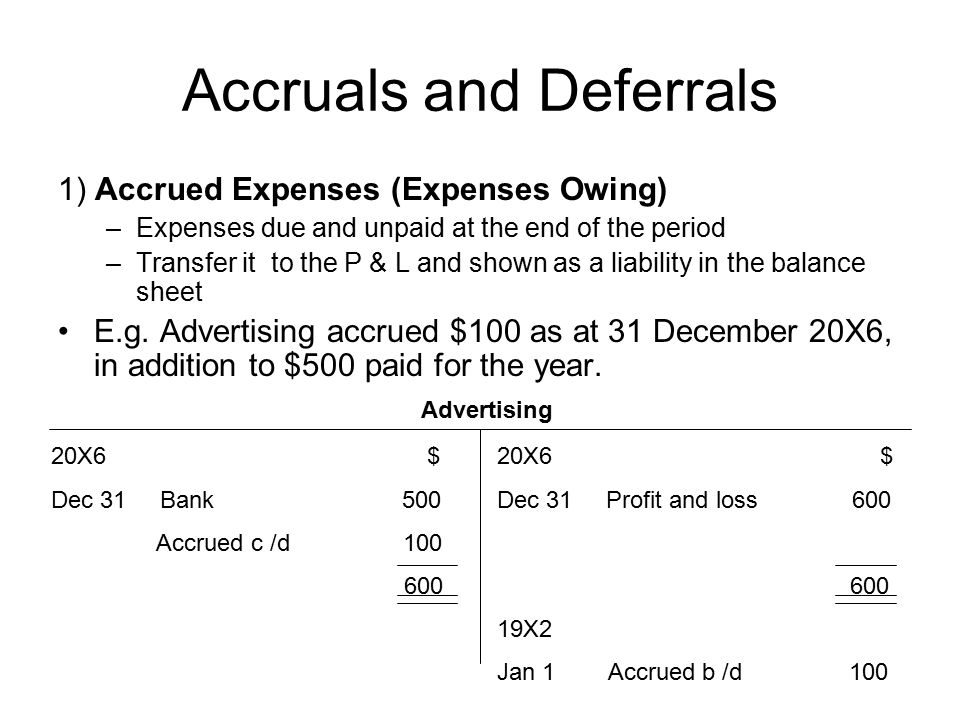

A small business that operates on accrual basis accounting matches up income and expenses into the period they are actually incurred, regardless of when money changes hands. This accounting method helps to improve the accuracy of a company’s reported net income. Accounting entries are made to either accrue expenses to the current period that have not yet been paid or defer them to the next period if they were paid early. Accrued expenses include all purchases for anything other than assets that have not been paid for by the end of the period.

The accountant debits an asset account for accrued revenue which is reversed when the exact amount of revenue is actually collected, crediting accrued revenue. Accrued revenue covers items that would not otherwise appear in the general ledger at the end of the period. When one company records accrued revenues, the other company will record the transaction as an accrued expense, which is a liability on the balance sheet. Period costs, such as office salaries or selling expenses, are immediately recognized as expenses (and offset against revenues of the accounting period) also when employees are paid in the next period. Unpaid period costs are accrued expenses (liabilities) to avoid such costs (as expenses fictitiously incurred) to offset period revenues that would result in a fictitious profit.

Accrued revenues and accrued expenses are both integral to financial statement reporting because they help give the most accurate financial picture of a business. Accruals are revenues earned or expenses incurred which impact a company’s net income on the income statement, although cash related to the transaction has not yet changed hands. Accruals also affect the balance sheet, as they involve non-cash assets and liabilities. Accrual accounts include, among many others, accounts payable, accounts receivable, accrued tax liabilities, and accrued interest earned or payable.

They should be reconciled to ensure that the entries are correct and complete. The accrual basis of accounting is the concept of recording revenues when earned and expenses as incurred. The use of this approach also impacts the balance sheet, where receivables or payables may be recorded even in the absence of an associated cash receipt or cash payment, respectively.

Both accrual and account payable are accounting entries that appear on a business’ income statements and balance sheets. An account payable is a liability to a creditor that denotes when a company owes money for goods or services. Because the company actually incurred 12 months’ worth of salary expenses, an adjusting journal entry is recorded at the end of the accounting period for the last month’s expense. The adjusting entry will be dated December 31 and will have a debit to the salary expenses account on the income statement and a credit to the salaries payable account on the balance sheet.

Under generally accepted accounting principles (GAAP), accrued revenue is recognized when the performing party satisfies a performance obligation. For example, revenue is recognized when a sales transaction is made and the customer takes possession of a good, regardless of whether the customer paid cash or credit at that time.

When accrued revenue is first recorded, the amount is recognized on theincome statementthrough a credit to revenue. An associated accrued revenue account on the company’s balance sheet is debited by the same amount, potentially in the form ofaccounts receivable. When a customer makes payment, an accountant for the company would record an adjustment to the asset account for accrued revenue, only affecting the balance sheet. Accrued revenue is recorded in the financial statements through the use of an adjusting journal entry.

Accrued revenues are revenues that are earned in one accounting period, but cash is not received until another accounting period. Accrued expenses are expenses that have been incurred in one accounting period but won’t be paid until another accounting period.

Accrued revenue is the product of accrual accounting and the revenue recognition and matching principles. The revenue recognition principle requires that revenue transactions be recorded in the same accounting period in which they are earned, rather than when the cash payment for the product or service is received. The matching principle is an accounting concept that seeks to tie revenue generated in an accounting period to the expenses incurred to generate that revenue.

Accrued Expenses vs. Provisions: What is the Difference?

As a result, if anyone looks at the balance in the accounts payable category, they will see the total amount the business owes all of its vendors and short-term lenders. When the expense is paid, the account payable liability account decreases and the asset used to pay for the liability also decreases. Accrued revenue is recorded when you have earned revenues from a customer, but have not yet billed the customer (once the customer is billed, the sale is recorded through the billing module in the accounting software). Accrued revenue situations may last for several accounting periods, until the appropriate time to invoice the customer. Nonetheless, accrued revenue is characterized as short-term, and so would be recorded within the current assets section of the balance sheet.

Accrued revenues are revenues earned in one accounting period but not received until another. The most common forms of accrued revenues recorded on financial statements are interest revenue and accounts receivable. Interest revenue is money earned from investments, while accounts receivable is money owed to a business for goods or services that haven’t been paid for yet.

The entry for accrued revenue is typically a credit to the sales account and a debit to an accrued revenue account. Do not record any revenue accruals in the accounts receivable account, since that is reserved for trade receivables that are usually posted to the account through the billings module in the accounting software.

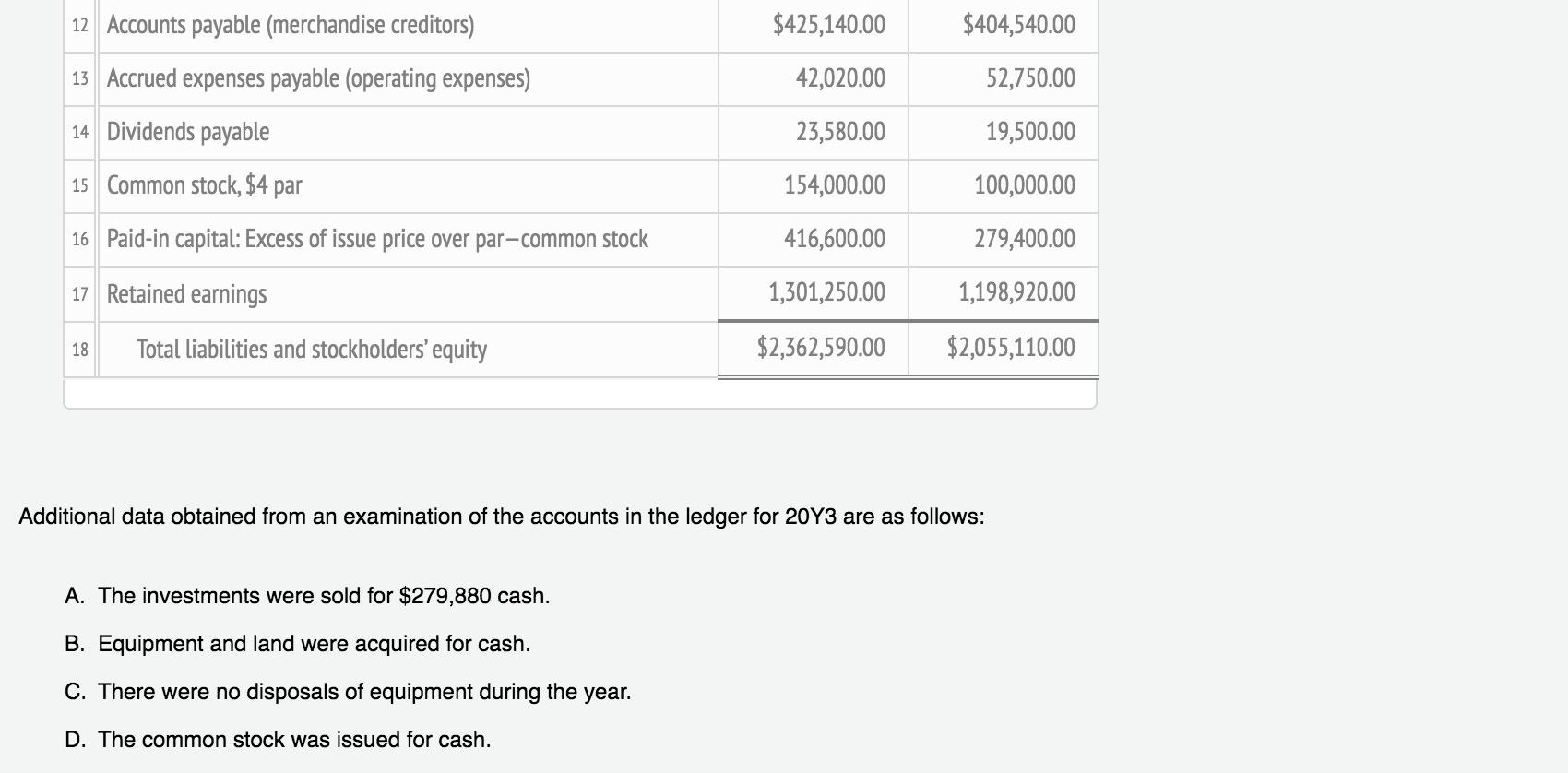

Accounts payable (AP), sometimes referred simply to as “payables,” are a company’s ongoing expenses that are typically short-term debts which must be paid off in a specified period to avoid default. They are considered to be current liabilities because the payment is usually due within one year of the date of the transaction. Accounts payable are recognized on the balance sheet when the company buys goods or services on credit. Companies must account for expenses they have incurred in the past, or which will come due in the future. Accrual accounting is a method of tracking such accumulated payments, either as accrued expenses or accounts payable.

- Accrued revenues are revenues earned in one accounting period but not received until another.

- Interest revenue is money earned from investments, while accounts receivable is money owed to a business for goods or services that haven’t been paid for yet.

How Do Accounts Payable Show on the Balance Sheet?

Accrued expenses are expenses a company accounts for when they happen, as opposed to when they are actually invoiced or paid for. An accrual method allows a company’s financial statements, such as the balance sheet and income statement, to be more accurate. Under the accrual accounting method, when a company incurs an expense, the transaction is recorded as an accounts payable liability on the balance sheet and as an expense on the income statement.

Reading the Balance Sheet

An example is a commission earned at the moment of sale (or delivery) by a sales representative who is compensated at the end of the following week, in the next accounting period. Accrued expenses is a liability with an uncertain timing or amount, but where the uncertainty is not significant enough to qualify it as a provision. An example is an obligation to pay for goods or services received from a counterpart, while cash for them is to be paid out in a later accounting period when its amount is deducted from accrued expenses.

Accrued expenses are expenses that are incurred in one accounting period but won’t be paid until another. Primary examples of accrued expenses are salaries payable and interest payable. Salaries payable are wages earned by employees in one accounting period but not paid until the next, while interest payable is interest expense that has been incurred but not yet paid. There are two key components of the accrual method of accounting.

There are a few common types of accrued expenses and accrued revenues. Falling under the accrued expenses category are salaries payable and interest payable. Salaries payable are wages earned by employees in one accounting period but not paid until another accounting period.

Does accrued expenses go balance sheet?

Accrued expenses payable are those obligations that a business has incurred, for which no invoices have yet been received from suppliers. These payables are considered to be short-term liabilities, and appear under that classification in the balance sheet.

An accrued expense payable is recorded with a reversing journal entry, which (as the name implies) automatically reverses in the following reporting period. By recording the expense in this manner, a business accelerates expense recognition into the current period. These payables are considered to be short-term liabilities, and appear under that classification in the balance sheet.

AccountingTools

Below, we go into a bit more detail describing each type of balance sheet item. Accrued expenses payable are those obligations that a business has incurred, for which no invoices have yet been received from suppliers.

The most common method of accounting used by businesses is accrual-basis accounting. Two important parts of this method of accounting are accrued expenses and accrued revenues.

Accrued expenses are realized on the balance sheet at the end of a company’s accounting period when they are recognized by adjusting journal entries in the company’s ledger. Accrued expenses (also called accrued liabilities) are payments that a company is obligated to pay in the future for which goods and services have already been delivered. These types of expenses are realized on the balance sheet and are usually current liabilities. Accrued liabilities are adjusted and recognized on the balance sheet at the end of each accounting period; adjustments are used to document goods and services that have been delivered but not yet billed.

Accounts Payable

Accrued expenses are those liabilities which have built up over time and are due to be paid. Accounts payable, on the other hand, are current liabilities that will be paid in the near future.