The accounting equation is one of the most fundamental accounting concepts that underpin the entire double-entry system. All entries that are made in the debit part of the balance sheet must contain corresponding credit postings in the Balance sheet. This rule is also known as the balance sheet or accounting equation. What the accounting equation may be expressed as and why?

Basic version

The basic formula of the accounting equation can be seen below. Let’s analyze the accounting equation formula.

Assets: the value of all items owned by the company, they can be tangible or intangible, but they are all owned by the company.

Liabilities: all debts that a company is obligated to pay in the short or long term.

Equity: how much a business has raised by issuing shares (stocks) as well as retained earnings or losses of the company. Since shareholders are investing in the company, capital is perceived as an obligation of the company.

There is another way the accounting equation may be expressed as.

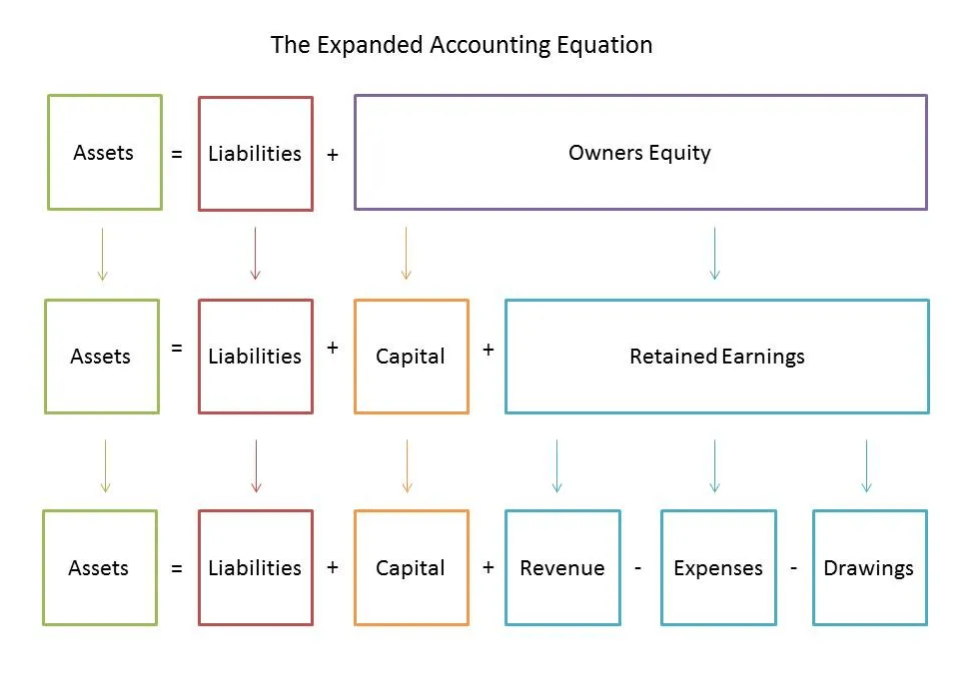

Expanded version

The following version is known as an expanded accounting equation. The extended version illustrates in more detail the various components of equity. Here, Owner’s equity is subdivided into the following elements:

Invested capital – capital provided by the original shareholders.

Retained earnings – income the business kept instead of distributing.

Revenue – what is generated as a result of the current activities of the company.

Expenses – expenses incurred to carry out the operations of a business.

Dividends (Drawings) – deducted as they are income distributed to the shareholders (owners).

The expanded version provides more details for the share capital portion of the standard accounting equation. This additional level of detail shows how the gains and losses from the Income statement are displayed in the equity section of the Balance sheet, and how cash outflows for dividend payments and share buybacks will reduce equity.

Uses

The equation is used by organizations to see a complete as well as a detailed picture of financial position. It can be used for a deeper study of the organization’s financial transactions and detailed analysis of financial statements. Basically, it shows the impact of each transaction that takes place and how it affects the liabilities and assets that an organization can have. In addition, it also describes in detail the aspects of any increase in cash flows from the money received or any decrease due to expenses incurred.Finally, today it is difficult to imagine a company that does not use the principles of double-entry, so it is important to know the different ways the accounting equation may be expressed as.