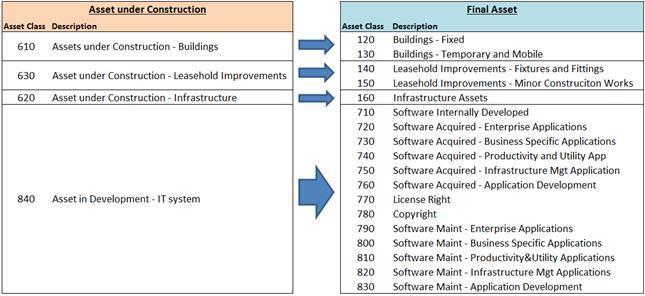

Leasehold improvements have different depreciation rules depending on whether you are working with U.S. tax basis financial reporting or the U.S. generally accepted accounting principles (GAAP) financial reporting. For tax purposes, leasehold improve…

Bookkeeping 101

What is the reciprocal of 7?

The first step in finding the reciprocal of a number is to make it into a fraction. For example, the whole number 8 can be made into the fraction 8/1. Once you have a fraction to work with, just flip the fraction upside down to find the reciprocal. T…

How to Prepare Financial Statements

The income statement is one of the financial statements of an entity that reports three main financial information of an entity for a specific period of time. Those information included revenues, expenses, and profit or loss for the period of time….

Omission

Using a 301 redirect is also a better solution than deleting the page completely because it will pass the link equity to page A. However, with a 301, page no. 2 will pretty much get deindexed so no page will be ranking for keyword no. 2 anymore….

What REALLY Happens if You Don’t File Your Taxes

Unexplained deposits can be considered taxable income if you can’t prove the nontaxable source, such as a gift or nontaxable sale of assets. Be prepared with an answer to these inevitable questions….

CMA Program

IMA provides a forum for members by promoting forward-thinking research and industry best practices and offering newsletters and journals. Each year, Institute of Management Accountants (IMA) conducts a global salary survey to discover trends in comp…

Definition of normal range

The CDC reported that “cluster[s] of negative attitudes and beliefs motivate the general public to fear, reject, avoid, and discriminate against people with mental illnesses”. The French sociologist Émile Durkheim indicated in his Rules of the Sociol…

Sales Revenue

For example, many companies list operating income separately, which is the money earned from a company’s core business operations. Conversely, non-operating revenue is the money earned from secondary sources, which could be investment income or proce…

Revenue Definition

But getting a grasp on these concepts is the first step toward evaluating your company’s efficiency and profitability. The revenue number is the income a company generatesbeforeany expenses are taken out. Therefore, when a company has “top-line growt…

Working capital in valuation

One of the company’s crucial health indicators is its ability to generate cash and cash equivalents. So, a company with relatively high net assets and significantly less cash and cash equivalents can mostly be considered an indication of non-liquidit…